Franc Goertz expands asparagus cultivation against the trend:

“We still need to ensure sufficient asparagus for supermarkets and other customers”

At Goertz Asperges in Maria Hoop, preparations for the asparagus season are in full swing. “We now have two-thirds of our acreage under black foil. Around 20 March, we expect to harvest the first asparagus. The rest of the acreage will follow later in the season, for harvest in April,” says Franc Goertz, who has been growing asparagus on the sandy soils of Limburg since 1987.

New sorting location for asparagus under construction

Against the trend, he has chosen to expand his asparagus acreage again this year. “We didn’t do it last year, but we are going to make up for it now. We still have to ensure that we have enough product left for the supermarkets and other customers,” the grower states. He expects a reasonably good harvest this season. “Last year, production was low, but last summer was reasonably good. However, we do see that many plots have not yet recovered from the flooding two years ago.”

“We see that it is not easy to maintain sufficient acreage in the Netherlands. Many small growers are stopping, and larger growers are no longer expanding as quickly, so the total area continues to decline slightly. There are several reasons for this. A number of growers do not have access to enough fresh land. In addition, it is not easy for everyone to secure sufficient staff, and there is a group of older growers who do not have a successor,” Franc continues.

Sweet potatoes Goertz is also expanding sweet potato cultivation again this year. “We are now supplying the last sweet potatoes of the season, but we would eventually like to move towards year-round production. We see enough demand from supermarkets, as well as from retail and farm shops. Demand increases slightly every year. Next year, we hope to deliver through until July.”

While Goertz initially grew sweet potatoes in two rows per bed, the plants are now grown on a small potato ridge. “We believe the plants warm up faster and deliver a higher yield,” says Franc. “Every year, the quality of Dutch sweet potatoes improves. It has to, because I want to be able to compare the product with the American ones; after all, these are the very best available on the market.”

Franc with his family

For Goertz’s third crop, blueberries, he has no plans to expand. “We are maintaining our plantation, but not increasing it. Last year, the harvest and price of blueberries were good, but it is and remains a difficult crop because it is so easy to transport. You can ship blueberries over long distances, and they can be supplied more cheaply from abroad. Our main crop remains asparagus, sweet potatoes are a product on the rise alongside it, and we are keeping blueberries stable.”

Antonio Zamora, director general-comercial de la Cooperativa Centro Sur:

“Calculamos que las inundaciones mermarán entre un 5 y 10% la cosecha de espárrago en Granada”

La Cooperativa Centro Sur ha realizado una primera valoración técnica del impacto provocado por la reciente borrasca en las plantaciones de espárrago del Poniente Granadino, situando las pérdidas estimadas en torno al 35-40% en la campaña 2026 en las zonas más afectadas.

“Evidentemente, hay parcelas que están completamente anegadas con un metro de tierra, donde recuperar la plantación va a ser muy difícil. En otras, que va a ser un poco más fácil recuperarla”, explica Antonio Zamora, director general-comercial de la cooperativa. “De hecho, ya están saliendo los primeros espárragos en fincas en las que el impacto ha sido menor”. En este sentido, Zamora destaca que estas lluvias ayudarán a tener una mejor cosecha a la mayoría de plantaciones que no han sufrido las inundaciones.

“El impacto global sobre el volumen total podría situarse preliminarmente entre un 5% y un 10%, inferior al previsto inicialmente, aunque aún es pronto para disponer de una evaluación definitiva de los daños, ya que muchas parcelas siguen siendo de difícil acceso y la evolución agronómica será determinante en las próximas semanas”, señala Zamora.

Centro Sur estima que entre 300 y 350 hectáreas se han visto afectadas por las inundaciones, sobre un total de 1.526 hectáreas cultivadas por la cooperativa.

Las zonas más afectadas se concentran en la ribera del río Genil y en el entorno del Arroyo Milano, especialmente en el municipio de Huétor Tájar, donde algunas plantaciones han permanecido inundadas entre diez y doce días. La bajada progresiva del nivel freático y del cauce del río está permitiendo que el agua se retire de parte de las parcelas, aunque persisten zonas donde el acceso sigue siendo complicado y dificulta una evaluación más precisa.

La campaña 2026 del espárrago acaba de comenzar, y los agricultores confían en que no se registren temperaturas elevadas, para que el exceso de agua pueda drenar correctamente y la planta comience a transpirar en condiciones óptimas. “Es un cultivo perenne y el tiempo de permanencia del agua en el suelo resulta determinante para evaluar tanto la merma productiva inmediata como el posible impacto estructural en campañas futuras”, indica Zamora.

Plan de recuperación de un sector estratégico para la economía del Poniente Granadino La Cooperativa Centro Sur subraya que el espárrago constituye un cultivo estratégico para el Poniente Granadino y para municipios como Huétor Tájar, donde genera empleo directo en campo y en los centros de manipulado y procesado, además de actividad económica indirecta en toda la comarca. Por ello, insiste en la importancia de analizar la situación con responsabilidad, evitando alarmismos pero también reconociendo el impacto que este episodio meteorológico ha tenido sobre el sector, los agricultores y sus familias.

“En este momento, el corazón de la Cooperativa Centro Sur está con los agricultores que están sufriendo las consecuencias de las recientes inundaciones. Queremos trasladarles todo nuestro apoyo y solidaridad, y reiterar nuestra disposición para acompañarlos y respaldarlos en esta situación tan complicada”, señala Antonio Zamora.

De hecho, desde el primer día, la entidad ha activado un plan de recuperación orientado a minimizar el impacto y apoyar directamente a los agricultores. Se están llevando a cabo trabajos de limpieza de caminos rurales para restablecer accesos a las explotaciones, así como la instalación de bombas para drenar el agua acumulada en aquellas parcelas donde no se evacúa de forma natural pese al descenso del nivel del río.

Además, se están aplicando tratamientos con hongos de suelo beneficiosos, una estrategia adoptada tras consultar con expertos de distintos países, que tiene como objetivo mejorar la transpiración y oxigenación de la parte radicular de la planta y favorecer el desarrollo del sistema radicular. La cooperativa subraya que estas medidas no ofrecen una garantía absoluta, pero confía en que puedan mitigar parte del impacto negativo. “La misión de nuestra empresa es generar riqueza en el mundo rural”, recuerda Antonio Zamora.

Llamamiento a las instituciones “Ahora bien, la ayuda no puede proceder solo del sector”, sostiene Antonio Zamora, quien reclama sensibilidad institucional ante una situación que puede afectar a puestos de trabajo directos e indirectos.

“En este sentido, solicitamos a las Administraciones que mantengan su apoyo al sector, mejoren las infraestructuras y estudien medidas que ayuden a mitigar el impacto productivo, especialmente en el caso de las organizaciones reconocidas como OPFH, Organización de Productores de Fruta y Hortaliza. Será fundamental habilitar mecanismos de ayuda para aquellos agricultores que pierdan plantaciones o sufran un fuerte deterioro en su medio de vida, así como para los trabajadores afectados”, afirma.

Por último, la Cooperativa Centro Sur quiere agradecer el interés y la implicación mostrados por el Gobierno de España, la Junta de Andalucía y la Diputación de Granada, y especialmente el trabajo diario del alcalde de Huétor Tájar, Fernando Delgado, y de todo el equipo humano del consistorio, así como la colaboración de la Unidad Militar de Emergencias, la Guardia Civil, la Policía Local y la solidaridad de todos los voluntarios que han prestado su ayuda durante los días más complicados.

“Queremos agradecer también a todo el equipo de Centro Sur su implicación en estos momentos de incertidumbre, volcados en apoyar a nuestros agricultores, así como la comprensión y el respaldo de nuestros clientes, que nos han acompañado y mostrado su apoyo desde el primer momento”, subraya Antonio Zamora.

White asparagus from Almopia, Greece, arrives one week later than usual

The Greek white asparagus cultivation season in Almopia, one of the key zones of this crop in Greece, is finally entering its last phase under favorable weather conditions, after the adverse weather that initially impeded the timely covering of the crops.

Mr. Christos Tripkos, general manager of Almopia Producers Association, says: “The rainy days of January caused a delay in the cultivation tasks, and we finally managed to cover our white asparagus in early February. Our cooperative manages 75 Ha, while in the whole area of Almopia, the asparagus crops extend to 250 Ha. In the middle of February, 20-25% of both our crops and the crops of the whole area remain uncovered. However, the weather has turned favorable. The night temperature is rising. We need it to stay above 0 degrees Celsius for the rest of February.”

The harvest beginning is estimated to take place in about two weeks from now. This means a one-week delay compared to the normal production calendar. According to Mr. Tripkos, “We will already be in the market by the beginning of March. If the March temperatures oscillate between 7 and 25 degrees Celsius, then we will have good productivity, despite the late start of the harvest. For us, it is essential to have already marketed at least 70% of our crop by April 10-15, because this is when the German asparagus arrives in great volumes on the German market, which is our target.”

The general manager of the Greek asparagus cooperative attended Fruit Logistica and was very satisfied with what was discussed there. As he comments, “The messages we are receiving are very encouraging. The demand is higher than last season. We have already proceeded with intention-based agreements with our German and Dutch clients, including Rewe, Edeka, and Aldi. We renewed agreements with all the companies we already collaborate with and also made agreements with new ones.”

“However, it is too early to speak about prices,” Mr. Tripkos stresses. “Prices are fixed every week for the following week. The first prices for the first March batches will be announced from February 25 to 28,” he concludes.

For more information: Christos Tripkos Almopia Producers Association Mob: +30 697 340 4343 Email: info@asparagus.gr Publication date: Fri 13 Feb 2026

« Nous estimons les pertes en asperges à 30 %, juste au début de la saison »

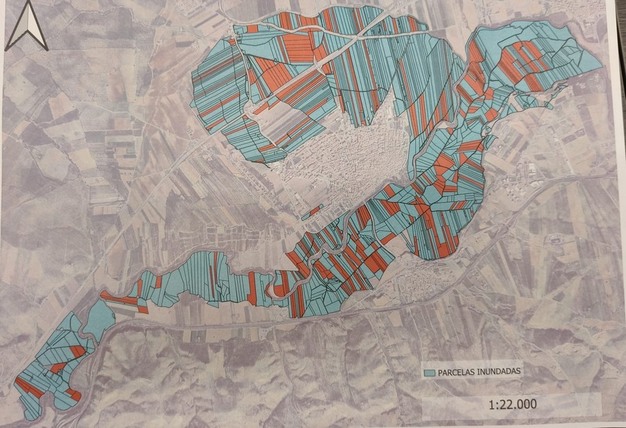

Près d’un tiers des cultures d’asperges vertes de la Vega Baja del Genil, principale zone de production de ce légume à Grenade et en Espagne, sont toujours inondées suite aux inondations qui ont particulièrement touché la commune de Huétor Tájar suite au passage de la tempête Marta. Le débordement du ruisseau Vilano et de la rivière Genil a causé d’importants dommages aux champs, aux canaux d’irrigation, aux infrastructures d’irrigation et aux communications, laissant la municipalité isolée par la route.

“Nous estimons qu’entre 25 et 30 % de la récolte d’asperges de Huétor Tájar a été perdue, ce qui représente environ 3 millions de kilos de produits, juste au début de la saison”, déclare José Antonio Gómez, membre du conseil d’administration de la coopérative Centro Sur. “Il pleut sur un sol déjà humide dans cette région, car nous avions accumulé beaucoup de pluie avant celles-ci”.

Carte des parcelles inondées autour de la municipalité de Huétor Tájar.

“Le démarrage de saison était imminent. En fait, les premiers lots situés dans les zones antérieures avaient déjà été récoltés, tandis que la zone inondée allait commencer à être récoltée dans une dizaine de jours”, souligne José Antonio Gómez. “Il s’agit sans aucun doute d’une perte importante qui ralentit la croissance de la superficie et de la production prévue pour cette année. D’un autre côté, d’autres zones de culture bénéficieront de la pluie”.

Débordements dans la ville de Huétor Tájar.

L’asperge est une culture clé pour l’économie locale, puisque près de 80 % de la population dépend directement ou indirectement de cette activité, qui compte plus de 2 000 coopératives membres et une appellation d’origine reconnue par l’Union européenne. Les inondations risquent donc d’entraîner la perte de nombreuses journées de travail au cours d’une saison qui s’étend principalement de mars à juin.

Les dégâts affectent particulièrement les zones de culture des asperges, mais les infrastructures hydrauliques historiques ont également été gravement endommagées, car les cours d’eau, détournés au début du XXe siècle, reprennent leur cours initial lors des inondations. Face à cette situation, le conseil municipal a demandé une aide d’urgence, la déclaration d’une zone gravement touchée et un programme spécial d’emploi agricole pour atténuer l’impact économique et social de la catastrophe.

Pour plus d’informations : Centro Sur, S.C.A Ctra. de la Estación, s/n. 18360, Huétor Tájar. Espagne. T : +34 958332020 info@centro-sur.es centro-sur.es

Reportage photo Fruit Logistica 2026 : des avis très hétérogènes côté français

Ce fut une édition résolument hivernale pour Fruit Logistica 2026, qui s’est achevée sous les pluies verglaçantes – une première selon quelques visiteurs historiques du salon interrogés par FreshPlaza Italie. Si les chiffres de cette année n’ont pas encore été dévoilés par les organisateurs, plus de 2 500 exposants de 90 pays (contre près de 2 600 exposants l’an dernier), étaient attendus du 4 au 6 février.

L’Italie, les Pays-Bas, l’Espagne, l’Allemagne et la France restent les cinq principaux pays représentés par les exposants, et la participation de l’Asie, du Moyen-Orient, de l’Afrique du Nord et de l’Afrique continue d’augmenter.

« Si les concurrents sont présents nous devons aussi y être » Si au fil des éditions, plusieurs entreprises françaises ont fait le choix de revenir en tant que visiteurs, d’autres ont maintenu leur présence en tant qu’exposants. L’édition 2026 a même enregistré l’arrivée de quelques nouveaux exposants français. Et alors que, ces trois dernières années, le constat revenait régulièrement sur une fréquentation jugée assez décevante, cette année plusieurs exposants du Hall 6.2 indiquent avoir été « agréablement surpris » par l’affluence. Pour beaucoup, Fruit Logistica reste un passage obligé : « si les concurrents sont présents, nous devons l’être aussi », confie trois d’entre eux. Un rendez-vous nécessaire pour entretenir la relation avec les clients existants, même si le salon apparaît aujourd’hui « moins propice à la création de nouveaux contacts commerciaux ».

Parmi les nouveautés aperçues au salon : nouvelle variété, nouvelles marques mais aussi nouvelle gamme sans oublier quelques nouveaux partenariats (article à venir). Les sujets de discussion les plus abordés dans les allées cette année : difficultés à produire (hausse coûts de production, distorsions de concurrence, phyto…) et marché en berne.

Dans le pavillon français, l’Interprofession, qui souffle ses 50 bougies cette année (créée le 10 juillet 1976), a mis en avant le ‘French Style’.

Fruit Logistica Innovation Award 2026 : qui sont les gagnants ? Cette année le FLIA, qui fête ses 20 ans, a été attribué à Pompeur, la marque de pomme hypoallergénique, dans la catégorie Fresh Produce, ainsi qu’au drone agricole L50 Drone d’ABZ Innovation, équipé d’un système de pulvérisation basé sur la technologie lidar.

Développée par Niederelbe, une entreprise basée en Basse-Saxe, Pompur est la première marque de pommes au monde certifiée par la Fondation européenne pour la recherche sur les allergies (ECARF). Le nom est composé des racines « Pom » (pomme) et « Pur » (pur). Cette pomme se distingue par sa couleur rouge croquante et par ses qualités gustatives.

Le L50 Drone remporte lui la catégorie technologie la plus innovante. L’entreprise hongroise ABZ Innovation, possède une batterie haute performance ainsi qu’un système de contrôle intelligent lui permettant de rester en vol beaucoup plus longtemps que les appareils comparables, couvrant jusqu’à 24 hectares. Disposant aussi d’un réservoir de 50 litres, le drone L50 convient aux exploitations agricoles ayant de grandes surfaces.

Espagne : les mauvaises conditions météo réduisent considérablement la disponibilité des fruits rouges

L’offre de fruits rouges en provenance d’Espagne reste limitée en raison du mauvais temps qui sévit dans la majeure partie du pays. Les exportateurs espagnols éprouvent de grandes difficultés à satisfaire la demande actuelle et celle des prochains jours, en vue de la Saint-Valentin.

“La saison des fraises a bien commencé en décembre, mais à partir du milieu du mois, il a commencé à faire plus froid que d’habitude et il a commencé à pleuvoir par intermittence, pendant plusieurs jours d’affilée jusqu’à maintenant”, explique un producteur et exportateur de Huelva.

“Avec une telle instabilité météorologique, la production progresse plus lentement et, en général, l’excès d’humidité provoque une plus grande destruction dans les champs. Nous effectuons une sélection plus minutieuse des fruits, ce qui se traduit par une baisse des volumes commerciaux et une augmentation des coûts”, explique-t-il.

En conséquence, la demande en Europe est supérieure à l’offre, car d’autres pays comme le Maroc et la Grèce connaissent également des problèmes météorologiques, ce qui fait grimper les prix.

“Les prévisions annoncent un temps instable pour les prochains jours, je ne pense donc pas que nous pourrons couvrir la demande pour la campagne de la Saint-Valentin”, avance l’exportateur. Les ventes de fruits rouges ont tendance à augmenter à l’approche de la Saint-Valentin”, rappelle-t-il.

“Bien que, pour l’instant, les conditions météorologiques aient été le plus grand défi de cette saison, nous espérons qu’elles se stabiliseront bientôt afin que nous puissions progresser de manière satisfaisante”, conclut-il. Date de publication: jeu. 29 janv. 2026

VENTE/TRANSMISSION d’une EXPLOITATION AGRICOLE Le producteur des Chefs part à la Retraite Asparagiculteur depuis plus de 30 ans sur la Commune de Mallemort dans les Bouches du Rhone cherche son successeur pour son exploitation rentable avec ses 2 activités principales : Asperges vertes et production de semences hybrides lui permettant la rotation des cultures et un bon équilibre des sols. Avec un chiffre d’affaire de : pour les asperges en 2025 de : 126 908.00 € HT pour une superficie de 2ha Autres cultures : pois chiches récoltés verts 14 400€ pour 1 ha en 2025 petits pois récoltés très fin 24 200€ pour 0.4 ha en 2025 pour la multiplication des semences hybrides : 58 800.00 € HT (minimum) sur 19 ha . Commercialisation

La production de semences est vendue sous contrat avec des coopératives

La production des asperges, petits pois, pois chiches verts et secs est vendue en direct sur l’exploitation à hauteur de 10 %, 10 % sont commercialisés aux primeurs alentours et 80 % au réseau de restaurateurs étoilés et non étoilés dans toute la France ,clients depuis de nombreuses années. (Le cédant proposait également jusqu’à l’année dernière, des mini-légumes à ce réseau qui serait en demande. Il a arrêté cette production dans le soucis de réduire son activité.) Foncier : 30 ha en location dont 1 ha de tunnels Toutes les terres sont à l’arrosage réseau collectif basse pression avec un prix forfaitaire de 110€/ha par an. Le personnel : motivé, formé et sérieux sous contrats saisonniers Prix de cession 268 000.00 € HT comprenant le matériel, les plantations d’asperges encours de production, le réseau clientèle. Accompagnement proposé par l’exploitant Contact : l’Exploitant Didier FERREINT 06 03 61 13 16 www.aspergesvertesmallemort.com aspergemallemortdidierferreint Asperges vertes de Mallemort

La saison des myrtilles de Larache démarre en force

Les myrtilles marocaines, notamment celles de la région nord de Larache, arrivent sur le marché avec trois semaines de retard par rapport à la saison dernière. Les volumes sont encore modestes, mais les producteurs s’attendent à ce que la production totale dépasse celle de la saison dernière grâce à une augmentation marquée des surfaces cultivées.

Zouhir Disouria de Global First Green Land, producteur et exportateur basé à Larache, déclare : “Le développement des fruits a été ralenti par la combinaison d’un temps froid, de pluies constantes et d’un ensoleillement réduit. Les premières récoltes sont également limitées en volume, ce qui rend le début de la saison progressif. Toutefois, nous sommes convaincus que les volumes et la qualité s’amélioreront progressivement jusqu’à l’arrivée du pic de récolte en mars.”

Les premières exportations ont déjà commencé, selon Disouria. “Nous avons envoyé nos premières cargaisons aux marchés asiatiques et à la Russie. La saison commence par des expéditions aériennes et des LCL, étant donné les petites quantités. Les plus grands producteurs expédient déjà des conteneurs complets. La forte demande en début de saison est de bon augure pour le reste de la campagne, selon le producteur. Il ajoute : “C’est une période chargée et nous recevons des demandes de devis de tous les marchés. Les acheteurs européens tâtent le terrain et se montrent très intéressés. Quant à la demande asiatique, elle est solide.

“Nous parvenons à obtenir de bons prix par rapport au début de la saison dernière, avec une augmentation de près de 15 % malgré la forte concurrence et les volumes encore disponibles sur le marché en provenance d’Amérique latine. Je pense que nos prix resteront compétitifs et se stabiliseront plus tard au même niveau que la saison dernière lorsque des volumes conséquents seront disponibles”, poursuit M. Disouria.

Le début de la saison est marqué par la poursuite des procédures d’exportation strictes imposées par les autorités marocaines chargées de la sécurité alimentaire. Ces mesures, introduites en 2024 et qui semblent désormais permanentes, visent à limiter les exportations par des négociants ponctuels et exigent des exportateurs qu’ils passent des contrats avec les producteurs. Disouria explique : “Les procédures marathoniennes comprennent également des analyses exhaustives qui augmentent les coûts. Chez Global First Green Land, nous avons la chance de pouvoir exporter notre propre production”.

“Nous serons présents à Fruit Logistica à Berlin en tant que visiteurs et nous nous réjouissons de discuter des perspectives de cette saison prometteuse”, conclut le producteur. Pour plus d’informations :

Every January, Aspa2 marks the start of the French asparagus season. Based in Indre-et-Loire, the company is one of the very first to market asparagus in France, kicking off a campaign that is eagerly awaited by market operators. This year’s harvest began on January 12th, under conditions that were deemed particularly satisfactory, both agronomically and commercially.

“Good sizes and quality” right from the start “We have good quantities and, above all, very good sizes for the start of the season,” explains a delighted Jacques Guironnet, the company’s managing director. Quality is once again at the heart of Aspa2’s priorities, with a product that fully meets the market standards. “We have a very white product, as we always strive to do. This is a very important criterion for us.”

Although the last few weeks have been marked by cold weather, this has not penalized production; quite the contrary. “On the one hand, our underground heating system protects us from the cold temperatures. In addition, we had some good vegetation this year, which enabled us to build up reserves in the autumn. It also explains the good sizes we have.” For a number of years, Aspa2 has relied on high-performance heating networks, enabling it to achieve remarkable earliness while ensuring regular production. A decisive advantage that explains its ability to reach the market well before spring.

An exceptional niche and a market to match In terms of marketing, the arrival of the very first French asparagus is always a big hit. “Customers are very happy to see the arrival of asparagus. It signals an early spring and, in the middle of winter, that is very good news.” In France, Aspa2 works mainly with wholesalers, but also generates a significant proportion of sales in exports, particularly to Asia, several European countries, and North America.

Being the first on the market is a definite advantage, even if this positioning corresponds to a very specific niche. “It is a production reserved for exceptional circuits,” admits the director. In terms of price, initial feedback has been satisfactory. “In a rather gloomy economic climate for many sectors, we are fortunate to be positioned in this particular niche.” On the strength of this momentum, Aspa2 is aiming to keep the campaign going right up to Easter, a key period for asparagus consumption. “We are enjoying good regularity in production, thanks to our fairly exceptional environmental conditions. So far, everything has been very positive, and we hope that the season will continue in this vein.”

For more information: Jacques Guironnet ASPA2 Phone: +33 (0)2 47 58 95 93 info@aspa2.fr www.aspa2.fr

Manage consent

To provide the best experiences, we use technologies such as cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Failure to consent or withdrawing consent may adversely affect certain features and functions.

Functional

Always active

Technical access or storage is strictly necessary for the legitimate interest purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

Technical access or storage is necessary for the legitimate interest purpose of storing preferences that are not requested by the subscriber or Internet user.

Statistics

Technical storage or access that is used exclusively for statistical purposes.Technical storage or access that is used exclusively for anonymous statistical purposes. Absent a subpoena, voluntary compliance from your internet service provider, or additional records from a third party, information stored or retrieved for this sole purpose generally cannot be used to identify you.

Marketing

Technical access or storage is necessary to create user profiles in order to send advertisements, or to track the user on a website or across websites with similar marketing purposes.

New sorting location for asparagus under construction

New sorting location for asparagus under construction

Franc with his family

Franc with his family For more information:

For more information:

Carte des parcelles inondées autour de la municipalité de Huétor Tájar.

Carte des parcelles inondées autour de la municipalité de Huétor Tájar. Débordements dans la ville de Huétor Tájar.

Débordements dans la ville de Huétor Tájar.